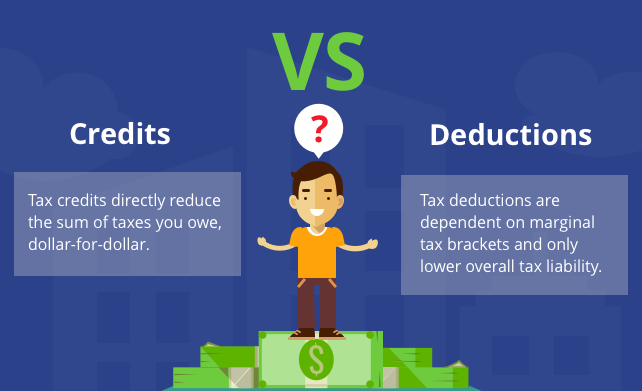

As tax season approaches, it’s important to understand the various tax deductions and credits available to you. Whether you are an individual or a business owner, several deductions and credits can assist you to save money on your tax bill. Uniform tax claim is an important concept every individual and business owner should know. It refers to claiming tax deductions and credits that can help reduce your tax bill. Here, we will explain some of the most common tax deductions and credits individuals and businesses can claim.

Personal Deductions: Reducing Taxable Income

One of the most useful methods to lower your taxable income is to claim personal deductions. You can deduct these expenses from your income before calculating your tax liability. Some of the most common personal deductions include contributions to retirement accounts, such as traditional IRAs or 401(k)s, mortgage interest, property taxes, and state and local income taxes.

It can be an important strategy for individuals looking to lower their tax liability. By claiming personal deductions, you can reduce your taxable payment, decreasing the tax you owe. It is important to keep accurate records of your expenses and contributions throughout the year to claim these deductions when it comes time to file your tax return.

Business Expenses: Deductions for Self-Employed Individuals

Self-employed individuals can also benefit from Uniform Tax Claims by claiming deductions for business expenses. These expenses are incurred while running your business and can be subtracted from your firm income to decrease your tax liability. Common business expenses include office supplies, equipment, travel, and insurance premiums.

Keeping detailed records of your business expenses throughout the year is important to claim these deductions. You should also consider working with a tax specialist to confirm that you are claiming all the beliefs that you are eligible for.

Charitable Donations: Tax Benefits for Giving

Charitable donations are another area where Uniform Tax Claims can be beneficial. If you donate to a qualified charitable organization, you can deduct the importance of the contribution from your taxable income. This can be a fabulous method to sustain a reason you care about while reducing your tax liability.

It is essential to mention that not all donations are tax-deductible. Additionally, there are limits to the number of charitable deductions you can claim each year, so it is important to keep track of your donations and consult with a tax professional if you have any questions.

Retirement Contributions: Planning for Your Future

Contributing to a retirement account is not only a wise economic decision but can also effectively reduce your tax liability. Contributions to traditional IRAs or 401(k)s are tax-deductible, meaning that you can subtract the payment of your grant from your taxable income.

Uniform Tax Claims can be particularly helpful for individuals who are planning for their future and want to save for retirement. By contributing to a retirement account, you can reduce your tax liability while also investing in your future financial security.

Education Credits: Deductions for Tuition and Fees

Finally, Uniform Tax Claims can also be beneficial for individuals who are pursuing higher education. There are several education-related tax credits and deductions that can help reduce the cost of tuition and fees..

Other education-related tax deductions include the Lifetime Learning Credit and the Tuition and Fees Deduction. Keeping accurate records of your education expenses is important to claim these deductions.

Energy-Efficient Upgrades: Credits for Homeowners and Businesses

If you’ve made energy-efficient upgrades to your home or business, you may be eligible for tax credits. The federal government offers several tax credits for energy-efficient upgrades, including solar panels, wind turbines, geothermal heat pumps, and more. These credits can offset the cost of your upgrades and reduce your tax liability. Additionally, many states offer tax credits and incentives for energy-efficient upgrades.

Child and Dependent Care: Credits for Working Parents

If you’re a working parent, you know that childcare can be expensive. Fortunately, tax credits are available to help offset the cost of childcare. The Child and Dependent Care Credit can assist you in preserving capital on your taxes if you paid for childcare for a child under age 13 or a dependent who is physically or mentally unable to care for themselves. The credit is based on a percentage of your childcare expenses, up to a maximum of $3,000 per child.

Healthcare Expenses: Deductions for Medical Costs

Medical costs can add up quickly, but tax deductions are available to help offset the cost. You can deduct medical and dental expenses that exceed 7.5% of your adjusted gross income. This includes expenses such as doctor visits, hospital stays, prescription medications, and more. Additionally, if you have a Health Savings Account (HSA) or a Flexible Spending Account (FSA), you may be capable of donating pre-tax dollars to help pay for medical expenses.

Investment Losses: Deductions for Capital Losses

If you’ve experienced losses in your investments, you can deduct those losses from your taxable income. Capital losses can offset capital gains, and if your losses exceed your gains, you may be able to deduct up to $3,000 in losses each year. Any losses above that amount can be carried forward to future tax years.

Homeownership: Deductions for Mortgage Interest and Property Taxes

If you possess a home, you may be eligible for tax deductions related to your mortgage interest and property taxes. You can subtract the interest you paid on your mortgage up to a maximum of $750,000 in mortgage debt. Additionally, you can deduct up to $10,000 in state and local property taxes. These premises can help decrease your tax liability and make homeownership more affordable.

Final Words

By handling the benefit of these tax breaks, you can diminish your tax liability and retain more of your hard-earned capital. So, explore these tax deductions and credits today and take advantage of the Uniform Tax Claim to help you save money on your taxes.

Uniform Tax Claim is an important concept that can help companies reduce their tax liability. You can lower your tax bill by claiming personal deductions, business expenses, charitable donations, retirement contributions, and education credits. It is important to keep accurate records of your expenses and contributions throughout the year and to consult with a tax professional that you are eligible.